Creditas financial results Q4-2023

São Paulo, 04th March 2024

Context of the business

2023 was a year of many accomplishments for Creditas. Despite keeping a conservative approach in terms of portfolio growth, we were able to deliver a 25% increase in top line (almost R$2.0bn annual revenues), that got transferred into an impressive 192% gross margin growth (R$640mn annual result) and 64% reduction of net losses (-R$385mn). In Dec-2023 we also achieved a very important milestone: operational breakeven. The combined effects of gross margin expansion through portfolio repricing and tight control of credit quality, improved cost efficiency and the positive tailwinds from a better macroeconomic cycle, enabled us to narrow net losses and set the foundation for a company that can start generating profit to reinvest in future growth.

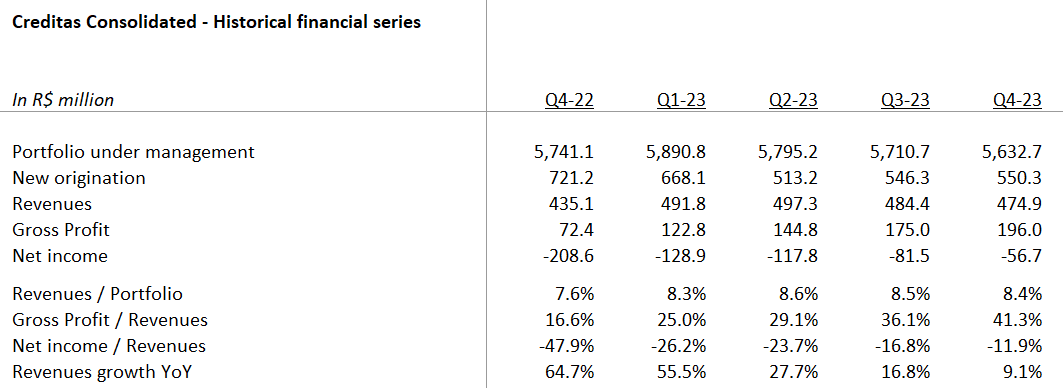

Hashing out about quarterly result, in Q4-23 we posted revenues of R$474.9mn, a 9.1% increase compared to Q4-22, and a gross profit of R$196.0mn, which represents a 171% increase vs. Q4-22. Gross Profit Margin as a % of revenues approached our 40-45% steady state level, moving from 12.1% 15 months ago to 41.3% in Q4-23, as we continued repricing of our loan book and maintained a high quality credit portfolio, which is delivering cost of credit at the lowest level since 2021. Costs below Gross Profit decreased compared to last quarter to R$253mn (-10.1% vs Q4-22) as we continue reducing CAC and gaining operation efficiency in the corporate structure.

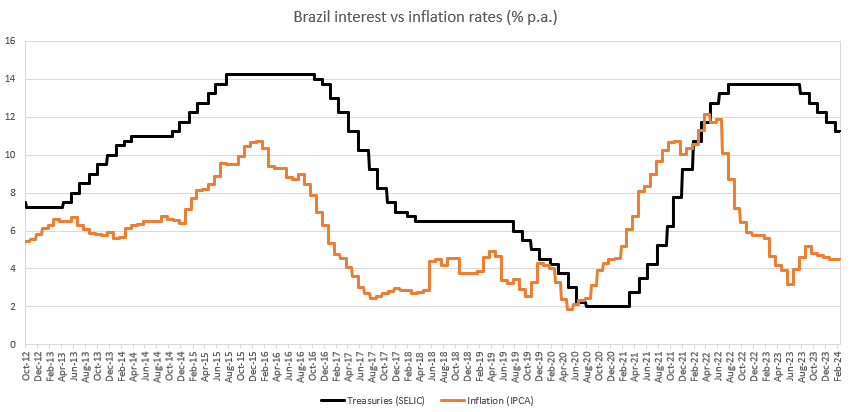

On the macro side, inflation ended 2023 at 4.62%, dropping by almost two-thirds since the peak observed in Apr-2022 at 12.13%. Future market expectations were positively impacted by this trend, currently projecting 3.82% IPCA for 2024 and 3.52% for 2025. SELIC closed 2023 at 11.75% and has already incorporated one more drop of 0.5% since then, endorsing the expectations of a continued decreasing trend, to reach 9.0% by the end of 2024. BRL has remained strong against USD, currently trading at 4.90-5.00, reflecting the steady decrease in Brazilian interest rate and controlled inflation, while the American economy faces a slowdown.

Following is an update on our action plan:

1. Keep portfolio growth high and sustainable: our portfolio remained almost stable vs a year ago (-2% decrease yoy), reflecting the tighter underwriting and a less aggressive approach to growth. In the next cycle, we will continue balancing growth and profitability so that portfolio growth provides future gross profit while keeping our eyes on the negative short-term impact related to growth (IFRS provision frontloading and customer acquisition cost).

2. Accelerate repricing of loan portfolio: pre-fixed loan pricing for new origination has remained stable at 62% in Q4-23, despite the drop in SELIC, aiming to accelerate gross profit expansion. Pre-fixed portfolio closed the year at 48%, increasing from 32% in Sep-21. This trend will continue through 2024 as we still have room for replacement of old portfolio by newer loans at new rates.

3. Increase gross profit: after gross profit compression during the second half of 2021 and early 2022 due to high growth (IFRS provisions impact), aggressive pricing to foster growth and rising interest rates (funding cost impact), we are now experiencing the reverse effect with gross profit achieving 40%+ gross profit margins, expansion from 12.1% in Q2-22 to 41.3% in Q4-23 (36.1% in Q3-23). The combination of loan repricing, a growing portfolio, stabilized cost of funding and lower IFRS provision impact creates significant tailwinds for profitability.

4. Acquisition of Andbank’s Brazilian banking operations: after signing the acquisition agreement in July 2022, Andbank completed the capital increase following the authorization from both Brazilian and European authorities, strengthening the balance sheet and accelerating deposit growth. The acquisition is in the process of approval by the Brazilian Central Bank.

5. Reduction of customer acquisition cost: we have managed to bring our customer acquisition cost to the minimum level ever thanks to (i) the impact of our automation efforts in both lowering acquisition costs and increasing conversion and (ii) returning users and repeating customers now representing most of our new loan origination. In addition, as our portfolio grows and loan repricing materializes, CAC represents a significantly lower portion of our revenues. On the other side, as we maintain tight credit policies and higher prices, we are facing some headwinds to further lower our CAC as conversion of our leads fall. As we move into a more neutral cycle in our business, we expect opening credit policies and lowering prices will progressively increase conversion and reduce CAC.

6. Rationalizing our overhead: with significantly reduced hiring after March 2022, we expect to continue increasing productivity per employee and gaining operational leverage.

7. Migration of Creditas Auto business model: After the change in the business model of Creditas Auto, we have focused on (i) reducing the existing inventory of cars which is now very close to zero and (ii) implementing our new C2C model (purchase of cars between individuals). We are seeing good initial traction on this new model but there are still many things that we need to develop to gain scale in the model.

Financial results

Quarterly results for the period Q4-2022 through Q4-2023

Operating performance

Q4-2023 revenues posted R$474.9mn compared to R$435.1mn in Q4-2022, a 9% increase despite the reduction in portfolio growth rates (-2% YoY reduction) and lower origination volumes (R$550mn in Q4-23 vs 721 in Q4-22). Portfolio under management reached R$5,633mn compared to R$5,741mn in Q4-2022.

We continue to be very restrictive in our Auto Finance product while mostly keeping our standard policies in Car Equity, Home Equity and Private Payroll loan products where we are seeing low volatility at this point in the cycle. Given the low loan-to-value of these products, we believe our product category is ideal to maintain resilience in the current environment.

After seeing our Gross Profit margins bottoming in Q2-2022 due to the impact of the sharp increase in SELIC and the impact of IFRS provisioning frontloading related to our high growth strategy, we are experiencing an acceleration in Gross Profit, which has increased 240% since Q2-2022 from 12.1% to 41.3%. Gross Profit benefited both from continuous loan portfolio repricing and lower cost of credit since, despite record-high inflation and interest rates, we have not seen a significant deterioration of credit quality and our portfolio remains highly resilient.

As a reminder, our Gross Profit margin is neutral to the level of interest rates in the economy but has compression and expansion depending on the speed of change in interest rates (impacting cost of funding while loan repricing lags due to the duration of our loan products) and speed of growth (impacting IFRS provisioning frontloading). The upward trend in Gross Profit started in Q2-2022, coinciding with SELIC rate reaching 13.75% after bottoming in Q1-2020 at 2.00%, and will continue during 2024, as SELIC is expected to continue falling. Decreases in SELIC rate will accelerate this return to historical average margins, which could already start to be seen in Q3-2023. As we mature as a company, we are creating the mechanisms to eliminate this fluctuation of margins in the long term by (i) issuing pre-fixed funding notes, (ii) increasing the portion of the portfolio with natural rate matching and (iii) having a clear framework to decide on the hedging of potential interest rate mismatches. We expect credit quality to remain strong during this part of the cycle, with additional tailwinds as the situation normalizes, interest rates trending down, and unemployment remains under control. The unemployment rate, which hovered at 12-15% in 2016-2021, has achieved the lower level since 2015 in the quarter ending Jan-24 at 7.6%.

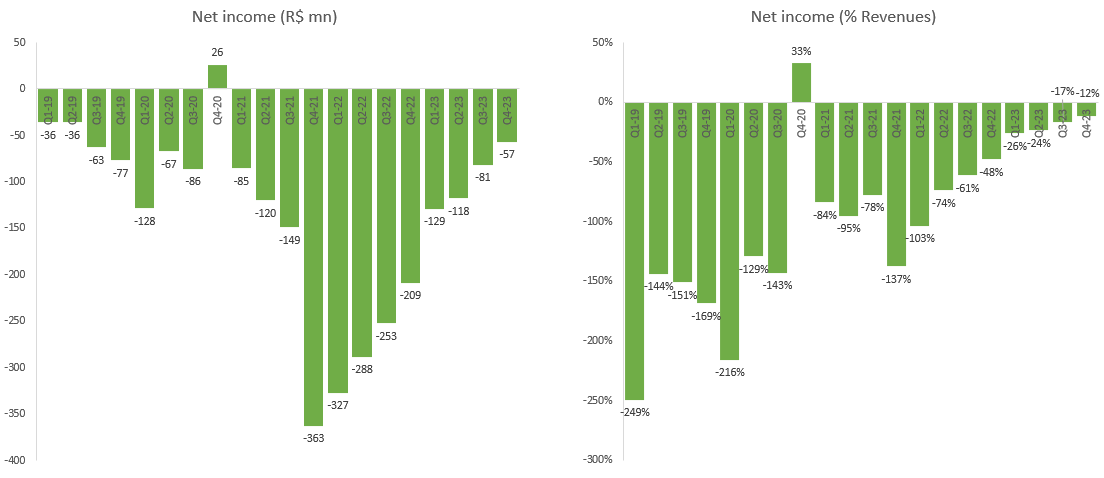

Over the last 12 months we have been able to increase gross profit from 17% to 41% (R$72mn to $196mn) thanks to portfolio repricing while keeping credit cost stable. We are optimistic about continuing these trends over the coming quarters towards our target steady state of 40-45% as our newly originated loans at higher prices increase the average portfolio profitability. The new phase of lowering SELIC will accelerate this process and we expect to be running at our steady-state gross profit levels in 2024.

In the chart below we overlap interest rates (SELIC) and inflation rates (IPCA). In the previous monetary cycle, when inflation reached 10.71% in 2016, SELIC stayed at 14.25% for 14 months; it took the BCB 9 months since inflation’s peak to start the interest rate reduction cycle. In the present cycle, it took 15 months since inflation peaked (12.13% in Apr-2022) to the BCB to start reducing interest rates, even after inflation had fallen to below 4%. Now, we expect this trend of falling interest rates to continue.

Below Gross Profit we recognize 3 types of costs: (i) Customer Acquisition Costs (CAC) that, despite generating gross profit over many years due to the long-term nature of the loans we originate, we recognize upfront, (ii) overhead costs, mostly related to product technology, a cost that unlike some incumbents, we do not currently activate and (iii) other financial income and expenses, as well as income taxes. As we continue building our portfolio, the impact of both CAC and overhead comes down on a relative basis as we get operational leverage thanks to scale. We expect to reduce both costs significantly over the next quarters as we continue growing our revenues and gross profit margins well above the evolution of CAC and overhead. All in, our path to profitability is related to (i) expanding gross profit related to stabilization of SELIC, portfolio repricing and lower impact of frontloading IFRS provisions, (ii) lower impact of customer acquisition cost as portfolio builds and we get higher efficiency in acquiring customers through our own user base and (iii) operational leverage as we continue growing our revenue base to absorb existing overhead that will grow at a significantly lower pace.

In Q4-23 we have continued to reduce both CAC and G&A costs, adapting to the new environment and with a clear focus of doing more with less. Costs below Gross Profit have come down to R$253mn in Q4-23 from R$281mn in Q4-22, a testament of the team’s focus on increasing productivity and efficiency. Our slower growth strategy for 2023 helped us to bring efficiency to our operation as we switched focus from hyper-growth (210% year on year growth in Q2-22) to moderate growth at this point of the cycle (9% year on year growth in Q4-23). With the company now on the right path to continue developing profitable growth, we will be refocusing our attention to long-term value-creation.

Thanks to this discipline around expenses, and despite the gross profit compression experienced with the increase of interest rates, we have been able to reduce our net losses from R$363mn in Q4-2021 to R$57mn in Q4-23. Despite some extraordinary items in Q4-2023 and some specific long-term investments carried out during the quarter, we reached profitability in December. As we accelerate the expansion of gross profit and continue gaining operational leverage, we are confident that we will keep a profitable growth throughout 2024.

***

Definitions

We present all our financials under IFRS (International Financial Reporting Standards). The key definitions of our financial and operating metrics are below:

Portfolio under management – Includes (i) Outstanding balance of all our lending products net of write-offs and (ii) outstanding premiums of our insurance business. Our credit portfolio is mostly securitized in ring-fenced vehicles and funded by both institutional and retail investors. Our insurance portfolio is underwritten by 14 insurance carriers.

New Origination – Includes (i) volume of new loans granted and (ii) net insurance premiums issued in the period. If new loans refinance outstanding loans at Creditas, new loan origination reflects only the net increase in the customer loan.

Revenues - Income received from our operating activities including (i) recurrent interest from the credit portfolio, (ii) recurrent servicing fees paid by the customers from the credit portfolio related to our collections activities, (iii) up-front fees charged to our customers at the time of origination, (iv) take rate of the insurance premiums issued, (v) other revenues from both lending and non-lending products. (Note: before Q2-2023 we were reporting revenues from cars sold which, giving the change in strategy, are not been included since Q2-2023 anymore; past numbers before Q2-2023 have been restated to make the series comparable).

Gross Profit- Gross Profit calculation adds or deducts from our revenues (i) funding costs of our portfolio comprising interest paid to investors and (ii) cost of credit including credit provisions and write-offs related to our credit portfolio which, under IFRS, are significantly frontloaded to account for future losses. (Note: given the shift in strategy, the cars marketplace margin is now considered as other income and expenses, below Gross Profit).

Net Income - Net income deducts from our Gross Profit (i) costs of servicing our portfolio, including headcount, (ii) funds’ operational costs (e.g., auditors, rating, administration fees, etc.), (iii) general and administrative expenses, including overhead, (iv) customer acquisition costs, (v) taxes, and (vi) other income and expenses. We currently don’t activate any of our technology investments which include third party providers, third party platforms and salaries of our product technology team.

Subscribe for

updates

Receive all our news in your email